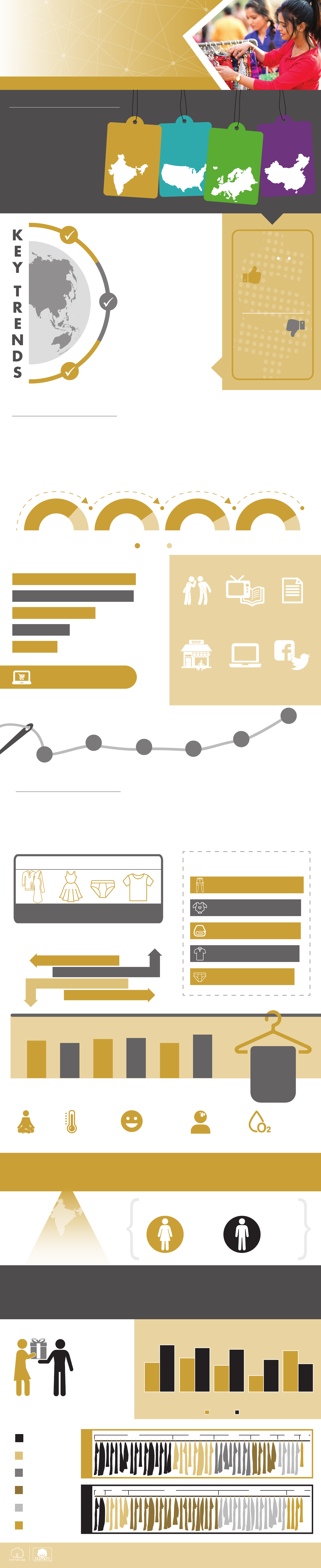

Spotlight on Gender

Differences: Meet the differing needs

of Indian women and men with product

offerings and retail experiences suited to

their shopping habits.

APPAREL SPENDING

What They Shop: Provide the

quality, fit, and durability

consumers seek with high

cotton-rich traditional clothing

and menswear.

FINANCIAL

OUTLOOK

90% 56%

OPTIMISTIC

How They Shop: Get ahead of online

shopping trends by investing in mobile

platforms while reaching today’s Indian

shoppers in-store and via traditional

media.

PESSIMISTIC

India Global

1% 11%

India Global

*”Neither Optimistic/Pessimistic”

not shown

GLOBAL CONSUMER

INSIGHTS

GLOBAL LIFESTYLE MONITOR: INDIA

US

$338.9

+56% growth

CHINA

$277.2

+193% growth

EU

$374.5

+52% growth

INDIA

$87.9

¹

+148% growth

Indian consumers spent $87.9

billion on clothing in 2017,

representing 6% of all consumer

expenditures. Spending on

clothing is expected to keep

pace with projected growth in

the economy overall, for a total

148% increase in clothing

expenditures by 2030. Seize

opportunities in this market with

online investment and cotton-rich

traditional clothing and menswear.

Window

Shopping

26%

Brand & Retailer

Digital Resources

24%

APPAREL SHOPPING HABITS

Buying Clothes on Impulse

Traditional

Media

54%

HOW THEY SHOP

Indian consumers are interested in shopping online, but with just 27% of the population using the internet

regularly (weekly or more)¹, lack of internet access prevents widespread online shopping. However, it’s

projected that 90% of the population will own a smartphone in the next 10 years¹, indicating a strong

future demand in mobile shopping. Small, independent shops and traditional street markets are frequent

shopping destinations, along with hypermarkets and department stores. Reach Indian shoppers in-store

and via traditional media while growing mobile platforms to meet future online shopping demands.

74% 80% 84% 84%

clothing research pre-purchase questions purchase repeat purchase

in-store online

SHOPPING JOURNEY

RETAIL STORES SHOPPED FOR CLOTHING

INDEPENDENT 67%

66%

45%

31%

24%

DEPARTMENT

HYPERMARKET

STREET MARKET

ONLINE ONLY

SOURCES FOR CLOTHING IDEAS

15%

Shop online at

least once per month.

Other

People

87%

Store

Publications

28%

Social

Media

22%

Consumers who prefer shopping in-store (vs. online)

33%

2008

40%

2010

46%

2016

77%

2018

36%

2012

35%

2 014

78%

Relieve

Stress

INTIMATES

JEANS & PANTS

PAY MORE FOR BETTER QUALITY

2008

77%

2010

73%

2 012

81%

2014

82%

2016

72%

2018

90%

DressesTrad. Attire Underwear

812 6 5

Average Number Owned

BABYWEAR

91%

WHAT THEY SHOP

Fit, durability, quality, and finish are important clothing factors to Indian consumers, and nine in ten choose

cotton-rich fabrics for garments of all types. Dresses and traditional clothing such as saris comprise nearly

half (43%) of women’s wardrobes, while men own both dress and casual pants and shirts. Indian

consumers value quality in clothing, as nine in ten are willing to pay more for quality. Offer high quality,

cotton-rich traditional clothing and menswear with a superior fit.

TOP ITEMS OWNED

COTTON AS PREFERRED FIBER

PERFORMANCE APPAREL

T-shirts

PRIMARY PURCHASE DRIVERS

FIT 89%

COMFORT 88%

QUALITY 88%

FINISH 88%

Likely to Purchase

HOME TEXTILES

91%

78%

Regulate Body

Temperature

91%

prefer cotton or

cotton blends

for their

most-worn

clothing

90%

93%

SHIRTS

86%

Consumers would like to know prior to purchase

76%

Monitor

Perspiration

76%

Monitor

Blood Oxygen

78%

Manage

Mood/Emotions

Men and women shop for clothing quite differently in India. While nearly all (95%) Indian women enjoy

clothes shopping, they break from the global trend as they report shopping for clothes less often than their

male counterparts. As just 27% of Indian women work outside the home² – among the lowest worldwide -

men are more likely to buy Western clothing in specialty and chain stores, while women frequent

tailor-made shops for traditional clothing. Adapt retail experiences to women and men with offerings suited

to their differing clothing and shopping preferences.

GENDER DIFFERENCES

IN SHOPPING

SPOT

LIGHT

Source: Cotton Council International and Cotton Incorporated’s Global Lifestyle Monitor Survey, a biennial consumer research

study. In the 2018 survey approximately 10,000 consumers (i.e. 1,000 consumers in 10 countries) were surveyed.

External Source: ¹Euromonitor International, ²WorldBank.

SHOP FOR OTHERS

WHAT’S IN THE CLOSET?

Percentage of Total Wardrobe

29%

India

51%

Globally

42%

India

44%

Globally

SHOP MONTHLY OR MORE

64%

54%

Men

Women

RETAIL STORES SHOPPED FOR CLOTHING

Significant Percentage Differences by Gender

Women Men

Specialty

20%

32%

Chain

23%

30%

Online

Only

18 %

29%

Factory

Outlet

11 %

22%

Tailor

Made

28%

19 %

Traditional Clothing

Intimates

Dresses & Skirts

Shirts

Pants & Jeans

Activewear

WOMENMEN

37

%

21

%

17

%

12

%

11

%

7

%

43

%

31

%

11

%

10

%

5

%